LINK: Profit Warning – Perspectives

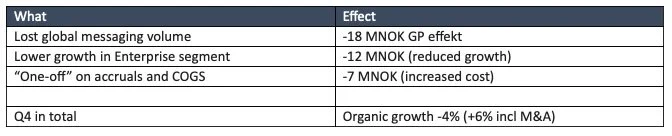

Yesterday, LINK issued a profit warning which pointed at a negative organic growth sized 4% in Q4 (+6% including SMS portal). They also communicated "we expect to return to growth during the coming quarters supported by solid CPaaS momentum and solid contract wins".

Facts

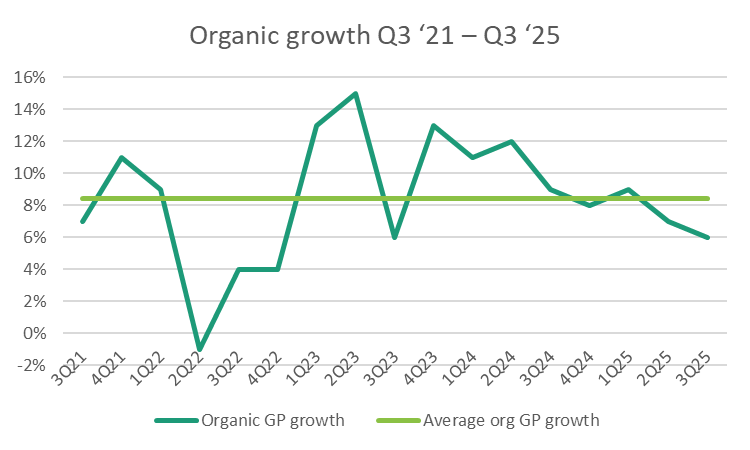

Question 1 - should quarterly volatility be expected?

If you take a look at our tabel page 9 in our analyses you'll see that organic growth volatility sometimes appear. We prefer "linear and stable" but it's not real world is it 🙂.

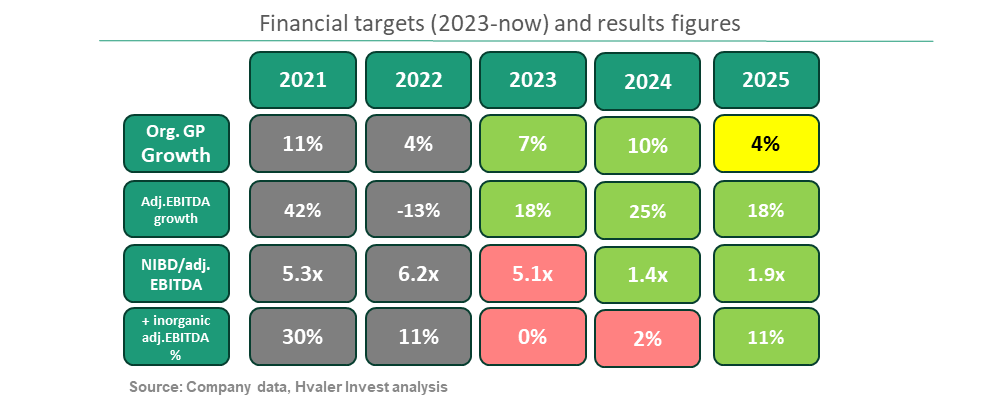

Question nr 2 - will company 2025 guiding hold or not?

The company guiding will hold. Organic growth is 4%. If you add the two other “green elements” the conclusion is high guiding credibility on an annual basis (which is the only thing that is important).

Question 3 - is the investment story still valid?

We would of course have preferred more detailed information from management yesterday, but we also understand that you need to draw a line and present the full story in the Q4 presentation February 12th. Our view is that the story is intact and we'll not sell a single share today (it's a promise).

Question nr 4 - what's the short and long term consequences of the profit warning?

These changes will reduce EBITDA with about 3.1%/2.5%/2.2 % in 2025/2026/2027 relative to Hvaler Invest analyses published December 1st. It leads to a limited reduction in company intrinsic value so our target price at NOK 58 will be modestly revised. We'll update you after spending some time to go through Q4 report ultimo Februar.

A reasonable reaction today is a 6–8% drop; a double-digit fall would be a buying opportunity. To put it into perspective it's not dramatic - is it?

Our conclusion - story intact

Quarterly volatility should be expected, company guiding credibility is good and the investment story is still intact. The compounding story have a small set back, but LINK are on track as we speak.

Let me share a secret - I have written a few profit warnings myself during my 60+ released quarterly reports. At "the end of the day" this company (Protector) have delivered 20% cagr growth and even better on annual shareholder return. No pressure Thomas, Morten and "team LINK" 🙂

Disclaimer: Hvaler Invest is a significant shareholder so you cannot trust us (or perhaps you can?

Best regards,

David and Sverre

Hvaler Invest AS

Lillestrøm, Norway

03.02.26