Morrow Bank buys MedMera Bank AB - Faster, Better, Higher

Illustration: AI generated

Who is MedMera and what are the buying terms?

MedMera is a Consumer Finance Bank in Sweden sized 66% of Morrow. It's owned by and closely linked to KF and COOP Sweden. Price is SEK 1.96 bn corresponding to 1.06x book value at closing date (early Q3) which is slightly lower than Morrows P/B today. Synergies are significant and will mainly be on buyers' side but will partly also benefit seller since approx. 10% of Morrow will be owned by the seller after closing. That future ownership to KF/Coop is also a positive since a distribution agreement follows the deal.

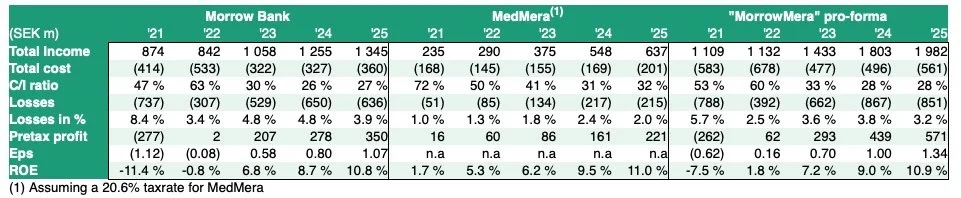

Let's look at a few figures last 5 years on the 2 banks:

Source: Hvaler Invest analysis

These figures tell a story about two fast growing Banks (total income CAGR 11% and 28% respectively since 2021), Scalability (C/I down from 47% to 27% for Morrow and from 72% to 32% for MedMera), stable losses and very fast-growing profits (CAGR 14% and 27% since 2023 respectively). The transaction is not about "solving problems" but "keeping momentum and seeking potential synergies" - is that your take as well?

Looking forward;

There are 2 main areas of interest:

Capital optimization. It will happen since i) Morrow now puts its extra capital to work quickly ii) MedMera adds AT1 and T2 capital capacity (none currently)

Cost synergies communicated at SEK 150 m. Both banks are scalable, and Morrow has demonstrated their ability to take out cost synergies lately. Combined they will move faster towards C/I sized 20%

There are a lot of other interesting areas, but if you trust management to deliver on these two, this is a no-brainer! An alternative view is that agent fee on a 11 BSEK organic portfolio is around 400 to 500 MSEK, so (a very rough guesstimate) 100 MSEK in one-offs to get this portfolio is peanuts.

You could argue for more upside and new opportunities for a Consumer Finance Bank now entering a no 3 position in the Nordic market but let's take that as a possible surprise if something turns out to be better than expected.

After Q4 (Feb 12th) we sent out an updated analysis on Morrow (+7% q/q growth and +25% y/y eps) and stated that our preferred option going forward was buying volume and not paying a dividend when moving the bank to Sweden and releasing a lot of capital. Now it's already happening, and it's moving faster and is bigger than we expected.

Conclusion; New target price not decided yet (previously 19.4 SEK) but will end higher

While waiting for more information and a potential prospectus, we like what we see. Morrow has turned around, are growing profitably, have moved to Sweden, released capital and are now putting that capital in to play through a significant transaction with limited risk where there are obvious cost- and capital - synergies. Price seems attractive since synergies are obvious, and Morrow Bank can now deliver better KPI's and higher profits at least 2 years faster than previously communicated. With strong support from majority owners and primary insiders (Kistefos AS and Belair AS) as well as others, we are supportive.

Management will give a presentation at 14:00. Follow this link to listen in; we will certainly do so.

Disclaimer:

Hvaler Invest is a significant shareholder so you cannot trust us (or perhaps you can?)

Best regards,

David and Sverre

Hvaler Invest AS

Lillestrøm, Norway

24.03.26