Morrow Bank analyse

7% q/q growth and eps up 25% y/y

Morrow Bank delivered another strong quarter where the Gross loan book is up 7% q/q including the MOANK acquisition sized SEK640M. Credit losses were stable at 3.9% and EPS landed at 0.30 NOK in Q4 (up 25% y/y). Management walk the talk - can you ask for more 🙂

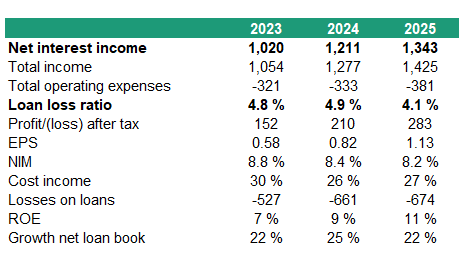

After Q4 we find it prudent to have a look at 2025 vs last 2 years. Here are a few selected figures:

Our expectation is a continued profitable growth based on i) high organic growth, ii) scalability, iii) a reasonable support from macro iiii) release of capital due to the Swedish banking license and possibly v) some portfolio acquisitions

We love the dividend communication since we agree on Morrow's capital priorities; 1) organic growth 2) M&A and 3) Dividends. We read this (rather unusual) dividend message towards "we are in a potential M&A dialogue as we speak" 🙂

Hvaler Invest’s target price is 20,9 NOK🔥and will probably not be changed after Q4.

Did you get a chance to see our Morrow Bank presentation and analysis last week?

👉 You can watch it, listen to it or read it here (PDF)

Disclaimer: Hvaler Invest is a significant shareholder so you cannot trust us (or perhaps you can?)

Best regards,

David and Sverre

Hvaler Invest AS

Lillestrøm, Norway

12.02.26